Prospects for Economic Integration in Indo-Pacific Region: A Perspective from Sri Lankaâ€ÂÂÂ.

Posted on March 27th, 2013

Press Release-Speech by Asanga Abeyagoonaskera, Executive Director, Lakshman Kadirgamar Institute (LKIIRSS) at the Annual Asian Relations Conference Organised by the Indian Council for World Affairs, New Delhi on March 22, 2013

Good Afternoon everyone, Rajiv K. Bhatia Director General ICWA, Prof. Swaran Sing, Guest speakers at the conference, distinguished ladies and gentleman.

ƒÆ’-¡ƒ”š‚ When I arrived in Delhi the headline on the Indian newspaper was “will Ceylon be a Cyclone for India”, been the only Sri Lankan at this conference I can assure you my country will always have a promising and a calm wind blown towards India, we wish the same from India. Only time it became a cyclone was when a Indian princess was stolen by a Sri Lankan. I quote our founder of the Institute, Lakshman Kadirgamar “India and Sri Lanka is lost in the mist of time” our culture and history is so much connected and both nations will need each other.

ƒÆ’-¡ƒ”š‚ This is the second time I am addressing at this prestigious Sapru House, which has a rich history of eminent scholars and world leaders participation. Last year at this same conference ICWA and Lakshman Kadirgamar Institute the premiere National think tank of Sri Lanka signed a MOU for collaboration. I wish to thank ICWA-AAS for inviting me for this important conference.

ƒÆ’-¡ƒ”š‚ The paper which I have co-authored with Amali Wedagedara, my Research Associate ƒÆ’‚¢ƒ¢-¡‚¬ƒ…-Prospects for Economic ƒÆ’-¡ƒ”š‚ Integration in Indo-Pacific Region: A Perspective from Sri LankaƒÆ’‚¢ƒ¢-¡‚¬ƒ”š‚ attempts to examine the nexus of ƒÆ’-¡ƒ”š‚ International Trade-Small Economies, particularly at the backdrop of a possible economic integration in the Indo-Pacific.

ƒÆ’-¡ƒ”š‚ Let me begin by sharing some thoughts about developments in South (China, India, Brazil, Indonesia, South Africa etc) from the Human Development Report 2013 released a few days ago. The compass is pointing to the Global South, never in the human history that so many lives have been improved, we are talking in billions. If you take the Industrial revolution Great Britain took 150 years to double its per capita and US took 50 years and in both countries only had a population of 10m at that time. ƒÆ’-¡ƒ”š‚ Today we have managed to double the per capita in 20 years in the South. This has contributed to ƒÆ’-¡ƒ”š‚ improve many lives more than 2 billion people is on this equation of growth. We have a tale of two worlds one a resurgent South and the other the North in crisis and unemployment.

ƒÆ’-¡ƒ”š‚ My presentation will first take a brief look at the Indo-Pacific, various possibilities it offer and different trajectories it could emulate. Then, it goes to study the prospects embedded the Indo-Pacific. After that, I will be studying the fate of small economies which will be discussed through the case of Sri Lanka. ƒÆ’-¡ƒ”š‚ Finally, I will share some suggestions both for small economies in South Asia as well as for India, in order to prepare themselves well for the upcoming developments in the regional order.

ƒÆ’-¡ƒ”š‚ As I pointed out, the next two decades will witness two distinctive drives in the world. Countries across the globe would be connected to China economically at an increasing phase. On the other hand, there will be a parallel drive towards as a provider of security and ƒÆ’‚¢ƒ¢-¡‚¬ƒ”¹…”insuranceƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢.

ƒÆ’-¡ƒ”š‚ In this environment, the ƒÆ’‚¢ƒ¢-¡‚¬ƒ”¹…”Indo-PacificƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢, is emerging as a geo-political and geo-economic space which encompasses both Indian and Pacific Oceans, a confluence of both outreach and interests of US, China, India, Japan, Australia.

ƒÆ’-¡ƒ”š‚ The former US State Secretary has articulated Indo-Pacific as an element of the US pivot to Asia. Shyam ƒÆ’-¡ƒ”š‚ Saran, ƒÆ’-¡ƒ”š‚ a ƒÆ’-¡ƒ”š‚ former ƒÆ’-¡ƒ”š‚ Indian ƒÆ’-¡ƒ”š‚ Foreign ƒÆ’-¡ƒ”š‚ Secretary ƒÆ’-¡ƒ”š‚ said ƒÆ’-¡ƒ”š‚ it ƒÆ’-¡ƒ”š‚ is ƒÆ’-¡ƒ”š‚ the ƒÆ’-¡ƒ”š‚ ƒÆ’‚¢ƒ¢-¡‚¬ƒ”¹…”logical ƒÆ’-¡ƒ”š‚ corollaryƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢ƒÆ’-¡ƒ”š‚ of ƒÆ’-¡ƒ”š‚ the broadening and deepening of IndiaƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s Look East Policy. Then, there are others who perceive it as an ƒÆ’‚¢ƒ¢-¡‚¬ƒ…-intersecting interests of the big maritime trading and strategic powersƒÆ’‚¢ƒ¢-¡‚¬ƒ”š‚.

ƒÆ’-¡ƒ”š‚ Since the Asian century has a lot to do with the rapid economic growth in the Asian region, particularly that of India and China, one may assume that the most prominent aspect or the driver of the Indo-Pacific would be economics ƒÆ’‚¢ƒ¢-¡‚¬ƒ¢¢”š¬…” economic relations between countries.

ƒÆ’-¡ƒ”š‚ What would be the forms these economic relations can assume? Would they go beyond bilateral Free Trade Agreements? Would there be new institutional set-up to accommodate them? Which countries would be the shapers of this new wave of regionalism? The present paper while answering some of these questions would attempt to bring in the perspective of a small country, Sri Lanka which is unlikely to play an active role in this regional drive.

ƒÆ’-¡ƒ”š‚ Indo-Pacific: Possibilities

ƒÆ’-¡ƒ”š‚ Advocated by ƒÆ’-¡ƒ”š‚ the Americans, Australians ƒÆ’-¡ƒ”š‚ and ƒÆ’-¡ƒ”š‚ the ƒÆ’-¡ƒ”š‚ Indians, ƒÆ’-¡ƒ”š‚ this ƒÆ’-¡ƒ”š‚ new ƒÆ’-¡ƒ”š‚ terminology ƒÆ’-¡ƒ”š‚ insinuates several ƒÆ’-¡ƒ”š‚ new ƒÆ’-¡ƒ”š‚ possibilities ƒÆ’-¡ƒ”š‚ and ƒÆ’-¡ƒ”š‚ trajectories ƒÆ’-¡ƒ”š‚ that ƒÆ’-¡ƒ”š‚ the ƒÆ’-¡ƒ”š‚ process ƒÆ’-¡ƒ”š‚ of ƒÆ’-¡ƒ”š‚ indo-pacific integration ƒÆ’-¡ƒ”š‚ could emulate.

ƒÆ’-¡ƒ”š‚ 1.ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ Depicted as an element of the USƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢ pivot to Asia, the ƒÆ’‚¢ƒ¢-¡‚¬ƒ”¹…”Indo-PacificƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢ could demand new commitments from the new rising powers in Asia in terms of sharing USƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢ burden in Asia (disseminate ƒÆ’-¡ƒ”š‚ and strengthen liberal democracy, human rights and free trade and share defence and military expenditure) 4.

ƒÆ’-¡ƒ”š‚ 2.ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ Affected by the Chinese military might and the rivalling political and strategic issues with China in terms of the territorial boundaries and access to sea lanes, aspirant regional powers would want to get together to contain China.

3.ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ Endorsing the very meaning of the term, it would be an inclusive and plural space where everyone can act to maximise their interests and utility through constructive engagement.

ƒÆ’-¡ƒ”š‚ As we know there are several contagious issues in the in the Asian region like the case of South China Sea which have the potential to flare up and de-stabilize the entire region. In this context, as the liberal trade theory might posit, regional integration is better go with the economic integration which would maximize common interests and seek to achieve a shared utility.

ƒÆ’-¡ƒ”š‚ What are the prospects for economic integration in the Indo-Pacific? Is there any space for a new institutional set-up? Or would it be a form of inter-regionalism with an umbrella organization housing parallel interests and agendas?

ƒÆ’-¡ƒ”š‚ Apart from bilateral FTAs, and other FTAs between ASEAN and other regional countries such as India, ƒÆ’-¡ƒ”š‚ China, ƒÆ’-¡ƒ”š‚ Korea ƒÆ’-¡ƒ”š‚ and ƒÆ’-¡ƒ”š‚ Japan, ƒÆ’-¡ƒ”š‚ Indo-Pacific region ƒÆ’-¡ƒ”š‚ has ƒÆ’-¡ƒ”š‚ more ƒÆ’-¡ƒ”š‚ than ƒÆ’-¡ƒ”š‚ ten ƒÆ’-¡ƒ”š‚ Regional ƒÆ’-¡ƒ”š‚ Economic CooperationƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ (RECs)ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ mechanisms. ƒÆ’-¡ƒ”š‚ WhileƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ mostƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ofƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ theseƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ arrangementsƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ haveƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ aƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ regional polarization, only Asia-Pacific Trade Agreement (APTA), with the membership of India, China, Bangladesh, Sri Lanka, Nepal, Laos, Philippines, and South Korea, seems to have encompassed membership from both South Asia and East Asia. Therefore, in our ƒÆ’-¡ƒ”š‚ opinion, there is still a possibility for an arrangement which would bring all these countries together.

ƒÆ’-¡ƒ”š‚ LetƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s look at various initiatives taken towards achieving economic integration in a regional set- up similar to the Indo-Pacific.

ƒÆ’-¡ƒ”š‚ With ƒÆ’-¡ƒ”š‚ the ƒÆ’-¡ƒ”š‚ objective ƒÆ’-¡ƒ”š‚ of ƒÆ’-¡ƒ”š‚ facilitating ƒÆ’-¡ƒ”š‚ closer ƒÆ’-¡ƒ”š‚ economic ƒÆ’-¡ƒ”š‚ ties, ƒÆ’-¡ƒ”š‚ a ƒÆ’-¡ƒ”š‚ step ƒÆ’-¡ƒ”š‚ towards ƒÆ’-¡ƒ”š‚ such ƒÆ’-¡ƒ”š‚ an ƒÆ’-¡ƒ”š‚ inclusive arrangement was made in 2007 when Japan suggested establishing a Comprehensive Economic Partnership for East Asia ƒÆ’-¡ƒ”š‚ (CEPEA), in order to deepen economic integration, narrow down development gaps, and achieve sustainable ƒÆ’-¡ƒ”š‚ development. It was supposed to be a free trade agreement between the current 16 member nations of the ƒÆ’-¡ƒ”š‚ ASEAN (ASEAN +China, Japan, South Korea + India, Australia, New Zealand) and attempted to achieve a more comprehensive integration than the ASEAN + 3 EAST ASIA Free Trade Area (EAFTA) proposed by China in 2001.

ƒÆ’-¡ƒ”š‚ Debate between CEPEA and EAFTA which continued for over two years ended in 2011 when the ASEAN proposed to formulate ASEAN centred FTA: Regional Comprehensive Economic Partnership (RCEP). ƒÆ’-¡ƒ”š‚ Negotiations for RCEP were launched in November 2012 during the 7th East Asia Summit and they are supposed to be concluded by the end of 2015. RCEP is expected to function with a liberal membership policy allowing any of the ASEAN FTA partner to join the forum whenever they wish to. In addition, any other external economic partner can also join the forum. A successful RCEP would be the biggest trade pact of the world incorporating 45% of the world population and would expedite the shift of global economic might towards Asia and ƒÆ’‚¢ƒ¢-¡‚¬ƒ…-would cover a combined economic output of US $ 20 trillion or almost one-third of the global economyƒÆ’‚¢ƒ¢-¡‚¬ƒ”š‚. Furthermore, the multilateralization process which RCEP will bring about would untangle the ƒÆ’‚¢ƒ¢-¡‚¬ƒ”¹…”noodle bowlƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢ resulted by the proliferation of FTAs in the Asian region.

However, the future of RCEP will depend upon the Future of the ASEAN Community which is expected to come to being in 2015. More than that, the intentions behind the initiations towards the RCEP will matter. If the intention behind these initiatives at regional integration is to co-opt geo-politicalƒÆ’-¡ƒ”š‚ rivals,ƒÆ’-¡ƒ”š‚ itƒÆ’-¡ƒ”š‚ couldƒÆ’-¡ƒ”š‚ bearƒÆ’-¡ƒ”š‚ negativeƒÆ’-¡ƒ”š‚ impactsƒÆ’-¡ƒ”š‚ onƒÆ’-¡ƒ”š‚ theƒÆ’-¡ƒ”š‚ globalƒÆ’-¡ƒ”š‚ economy. Therefore,ƒÆ’-¡ƒ”š‚ itƒÆ’-¡ƒ”š‚ is extremely important to make a comprehensive analysis of the ƒÆ’-¡ƒ”š‚ political motives behind such processes.

ƒÆ’-¡ƒ”š‚ Even though ƒÆ’‚¢ƒ¢-¡‚¬ƒ”¹…”greater welfare for allƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢ might be the ultimate objective of any form of regional arrangement, the process entails winners and losers to various degrees. Small states with much smaller economies and a little diversity would be the first and hard hit. On top of that other small countries in South Asia, with their backward approach to regional integration coupled with their protectionist trade policies, are less likely to be a part of a wider block.

ƒÆ’-¡ƒ”š‚ ƒÆ’‚¢ƒ¢-¡‚¬ƒ”š‚¢ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ What would be the economic consequences of Indo-Pacific on small states in South Asia?

ƒÆ’-¡ƒ”š‚ ƒÆ’‚¢ƒ¢-¡‚¬ƒ”š‚¢ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ How could they be supported and what can the new regional set-up do to mitigate their costs?

ƒÆ’-¡ƒ”š‚ By making an analysis of Sri Lanka-India economic behaviour, the paper attempts to examine the nature of impact a closer integration of the Indian market with the East Asia would have on Sri Lanka.

ƒÆ’-¡ƒ”š‚ Sri LankaƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s is a small open economy of almost US $ 60 billion in terms of the Gross Domestic Production (GDP) at market prices. When compared with other countries in South Asia, it is the fourth largest economy. Like most of the other South Asian countries, Sri Lanka is also a lower middle income country with per capita GDP of US $ 2, 836. While Sri Lanka is predominantly an agrarian economy, there has been a gradual shift towards the services sector in terms of the contribution to the national economy (59.5% in 2011). The industrial sector contributes 29.3% while the Agriculture accounts for only 11.2%.

ƒÆ’-¡ƒ”š‚ In post-2009 context, the overall economy has grown at around 7% annually, mainly driven by the strong domestic demand (Trade Policy Review: Sri Lanka 2010).

ƒÆ’-¡ƒ”š‚ In Sri Lanka, International Trade is a principal mode of market expansion, acquiring a greater integration to the world economy. Therefore, Sri Lanka pursues these objectives at different levels through three bilateral agreements; India, Pakistan and Iran, three regional agreements; South Asian Free ƒÆ’-¡ƒ”š‚ Trade Area ƒÆ’-¡ƒ”š‚ (SAFTA) ƒÆ’-¡ƒ”š‚ Agreement, ƒÆ’-¡ƒ”š‚ and ƒÆ’-¡ƒ”š‚ the Asia-Pacific Trade Agreement (APTA) and BIMSTEC.

ƒÆ’-¡ƒ”š‚ India-Sri Lanka FTA, which came into being in 2000, is the very first free trade agreement to both countries. It led to a new depth in economic relations of both countries by quadrupling the volume of bi-lateral trade. In the aftermath of the agreement, India emerged as Sri LankaƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s third largest export destination and the largest import destination.

ƒÆ’-¡ƒ”š‚ However, despite these, protectionist trends among the Sri Lankan business community as well as in the political class, partly due to various non-tariff barriers, red tape prevalent in the Indian economy, have hindered proceeding to the next level oftrade liberalisation between India and Sri Lanka; Comprehensive Economic Partnership Agreement which would be liberalising services and investment. In spite of Sri LankaƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s Free Trade Agreement with India, Sri Lanka accounts only 5% in Indian imports. Recently Bangladesh has replaced Sri ƒÆ’-¡ƒ”š‚ Lanka as the largest South Asian trade partner of India.

ƒÆ’-¡ƒ”š‚ In this backdrop, how would the developments regarding Indo- Pacific integration influence Sri Lanka? Sri ƒÆ’-¡ƒ”š‚ Lankan economy, the institutional set-up as a whole is very promising. Given the comprehensive ƒÆ’-¡ƒ”š‚ policy ƒÆ’-¡ƒ”š‚ framework ƒÆ’-¡ƒ”š‚ inclusive ƒÆ’-¡ƒ”š‚ of ƒÆ’-¡ƒ”š‚ fiscal ƒÆ’-¡ƒ”š‚ and ƒÆ’-¡ƒ”š‚ monetary ƒÆ’-¡ƒ”š‚ regulating ƒÆ’-¡ƒ”š‚ as ƒÆ’-¡ƒ”š‚ well ƒÆ’-¡ƒ”š‚ as infrastructure projects that various ƒÆ’-¡ƒ”š‚ governments have pursued in order to render Sri Lanka an attractive destination for FDI and International Trade, Sri Lanka is doing well in terms of various indexes, much better than other South Asian countries including India.

ƒÆ’-¡ƒ”š‚ For example, according to the Index of Economic Freedom 2013, Sri Lanka is categorized as

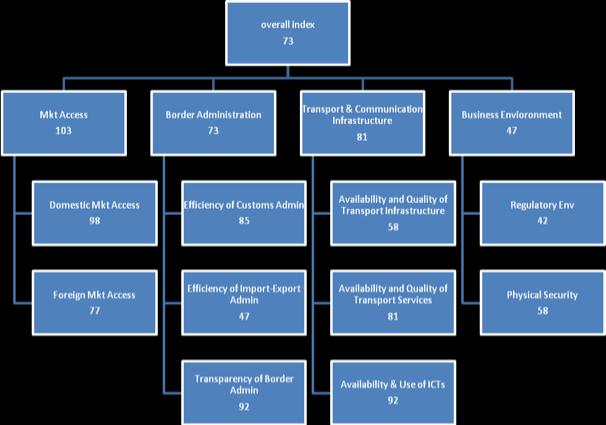

ƒÆ’‚¢ƒ¢-¡‚¬ƒ”¹…”moderately freeƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢ and is ranked 81 place. Enabling Trade Index of the World Economic Forum which uses seven pillars to determine the quality of trade policies in order to facilitate trade, ranks Sri Lanka at the 73rd in 2012.

ƒÆ’-¡ƒ”š‚

However, the sub-indexes of the Enabling Trade Index illustrated in this diagram above show some discrepancies.

ƒÆ’-¡ƒ”š‚ Even though, Sri Lanka pursues a stated policy of ƒÆ’‚¢ƒ¢-¡‚¬ƒ…-broadening the export base, diversification of export markets, increasing domestic value additions, and creating an enabling environment for trade to support the countryƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s ƒÆ’-¡ƒ”š‚ envisaged growth trajectoryƒÆ’‚¢ƒ¢-¡‚¬ƒ”š‚, Sri Lankan exporters seem to be having problems in accessing foreign markets due to issues faced by local exporters with respect to access to imported inputs at competitive prices, in identifying potential markets and buyers, in meeting quality requirements of the export market and access to appropriate ƒÆ’-¡ƒ”š‚ technology and skills.

ƒÆ’-¡ƒ”š‚ In addition, the sub-index of Transport and communication infrastructure also identifies gaps with regard to translating existing infrastructural facilities to actual services. For example, the index ƒÆ’-¡ƒ”š‚ rating ƒÆ’-¡ƒ”š‚ on ƒÆ’-¡ƒ”š‚ ƒÆ’‚¢ƒ¢-¡‚¬ƒ”¹…”availability ƒÆ’-¡ƒ”š‚ and ƒÆ’-¡ƒ”š‚ quality ƒÆ’-¡ƒ”š‚ of ƒÆ’-¡ƒ”š‚ transport ƒÆ’-¡ƒ”š‚ infrastructureƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢ is ƒÆ’-¡ƒ”š‚ not ƒÆ’-¡ƒ”š‚ reflected in ƒÆ’-¡ƒ”š‚ the ƒÆ’‚¢ƒ¢-¡‚¬ƒ”¹…”availability and quality of transport servicesƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢. Therefore, it must be noted that investments on improving infrastructure have to accompany a parallel process of enabling and empowering the population in order to overcome barriers in translating facilities available to services which people can enjoy for real.

ƒÆ’-¡ƒ”š‚ As much as the policy infrastructure, trade profile of a country is equally important to understand the behaviour of trade in a particular country. Given its colonial roots, Sri LankaƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s traditional export market continues to be the US and EU.

ƒÆ’-¡ƒ”š‚ About 56% ƒÆ’-¡ƒ”š‚ of ƒÆ’-¡ƒ”š‚ the ƒÆ’-¡ƒ”š‚ exports ƒÆ’-¡ƒ”š‚ are ƒÆ’-¡ƒ”š‚ concentrated ƒÆ’-¡ƒ”š‚ on ƒÆ’-¡ƒ”š‚ EU ƒÆ’-¡ƒ”š‚ and ƒÆ’-¡ƒ”š‚ NAFTA while ƒÆ’-¡ƒ”š‚ intra-regional ƒÆ’-¡ƒ”š‚ trade accounts only 9%. Other emerging markets in Latin America, ASEAN and Africa account only

2%, 7% and 2% respectively. Owing to the negative experiences of Sri LankaƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s exports to US and EU affected by the drastic impacts on the Global Financial Crisis the markets as well as political economic vulnerabilities developed from excessive dependence on the western markets have generated an interest to diversify Sri LankaƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s export markets. These reasons coupled with the rise of East Asia, have prompted a ƒÆ’‚¢ƒ¢-¡‚¬ƒ”¹…”Look East PolicyƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢ in the ƒÆ’-¡ƒ”š‚ Sri Lankan economic and political discourse as well.

ƒÆ’-¡ƒ”š‚ However, the fact that Sri Lanka doesnƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢t have any market access mechanisms in the East Asia except for APTA has emerged as an obstacle to exploiting the East Asian markets.

ƒÆ’-¡ƒ”š‚ On top of that, lack of a competitive advantage with respect to our products which are basically ready-made garments and a few manufactured goods have also affected Sri LankaƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s options. Almost all Sri Lankan exports are simple products which can be copied by other competitors, therefore risk further deterioration of the market options. In addition, value of high-tech products among the exports have also had a sharp drop from US $ 102 million in 2008 to US $ 57 million in 2010.

ƒÆ’-¡ƒ”š‚ Moreover, even though Sri Lanka has entered into several FTAs and RECs, Sri Lanka has failed to make a full utilization of these arrangements. Annual Report 2011 of the Central bank reports that bulk of Sri Lankan exports under APTA is limited to tea and coir products. Sri LankaƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s bilateral FTAs with India, Pakistan and Iran narrate a similar story. Although these agreements have accelerated bilateral trade in large volumes, Sri Lanka has failed to maximize the market access opportunities and tariff concessions by transcending its primary products.

ƒÆ’-¡ƒ”š‚ When Sri LankaƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s strategic advantage ƒÆ’†’ƒ”š‚ propos its exports lies in the western market, how economically sensible is it to take a shift towards the East? What is the way forward for Sri Lanka and India?

ƒÆ’-¡ƒ”š‚ 01. Make a critical evaluation of its geo-political location, how it can be used constructively

ƒÆ’-¡ƒ”š‚ Proximity to the Indian subcontinent as well as its location on strategic East-West Sea Lanes of Communications (SLOCS) is the biggest advantage to Sri Lankan in Indo-Pacific region.

Capitalising on Sri LankaƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s physical location and its natural harbours, the country is better placed than any other nation in South Asia to pursue the agenda of being a ƒÆ’‚¢ƒ¢-¡‚¬ƒ”¹…”transhipment hubƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢. At the moment according to the American Association for Port Authorities, Colombo port is one of the leading ports in the world and is ranked 80th in terms of the total cargo volume and the 29th in terms of container traffic in 2011. Colombo port handles ƒÆ’-¡ƒ”š‚ around 49,615 metric tons of cargo volume per year and 3,651,963 TEUs of container traffic annually. It is estimated that about 70% of the transshipment cargo in the container traffic in Colombo Port belong to India. Even in the face of a possible execution of the Sethusamudram plan, Sri Lankan ports will not be affected since the depth of the Sethu canal will not allow mega containers to pass through. Therefore, Sri Lanka ought to be mindful about this constant reality which is bound to bring greater benefits to Sri Lanka in the coming decades.

ƒÆ’-¡ƒ”š‚ 02. Integrate more with India

ƒÆ’-¡ƒ”š‚ Integrating more with the Indian supply chains is the best method that Sri Lanka could integrate with the global economy. The fact that India is an indispensable partner to Sri LankaƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s growth is further substantiated by the degree in which Sri Lankan economy depends on India. Apart from being a destination and a point of origin to transhipments in the Colombo port, India is also a major energy source to Sri Lanka. About 35% of Sri LankaƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s energy requirements come from India, through Lanka IOC. In addition, bulk of revenue generated in the Aviation industry comes from the weekly flights to India (42%). Furthermore, Indians account for the majority of tourists visiting Sri Lanka.

ƒÆ’-¡ƒ”š‚ These statistics reiterate the importance in untangling politics from the economic imperatives which would be vital in sustaining Sri LankaƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s growth story. First initiatives towards deepening integration in the Indian market ƒÆ’-¡ƒ”š‚ can be through further consolidating and utilization of the provisions available under the Indo-SL FTA.

03. Look at positives and look outward

ƒÆ’-¡ƒ”š‚ i.ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ Expanding and diversifying the export basket

ƒÆ’-¡ƒ”š‚ A bulk of the Sri Lankan exporters is from the Small and Medium sectors who deal with innovative products and services. ƒÆ’-¡ƒ”š‚ Improvement and expansion of these sectors are constrained by the scarcity of capital. Therefore proper policies to provide assistance to SMEs with potential such as light engineering products, plastic products, printing services, Toys and wooden furniture can revitalize the sector.

ƒÆ’-¡ƒ”š‚ ii.ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ Establish a nexus between the policy makers and business community

ƒÆ’-¡ƒ”š‚ Flow of information through a close relationship between the business community and the trade officers in the missions as well as in the Department of Commerce would benefit both communities. As much as it will help the producers in finding markets, the policy makers will be informed on the export capacities, nature of export products and sensitivities of the producers.

ƒÆ’-¡ƒ”š‚ Such close ƒÆ’-¡ƒ”š‚ interactions ƒÆ’-¡ƒ”š‚ between ƒÆ’-¡ƒ”š‚ the ƒÆ’-¡ƒ”š‚ governments, ƒÆ’-¡ƒ”š‚ chambers ƒÆ’-¡ƒ”š‚ and ƒÆ’-¡ƒ”š‚ other ƒÆ’-¡ƒ”š‚ trade ƒÆ’-¡ƒ”š‚ related organizations would help identify gaps and limitations in our trade policy, would assist innovations in order to ƒÆ’-¡ƒ”š‚ expand ƒÆ’-¡ƒ”š‚ our export portfolio and tap new and emerging export markets.

ƒÆ’-¡ƒ”š‚ 04. Look inward

ƒÆ’-¡ƒ”š‚ Nobel laureate economist Joseph Stiglitz states

ƒÆ’-¡ƒ”š‚ ƒÆ’‚¢ƒ¢-¡‚¬ƒ…-To be able to grow, emerging markets must be less dependent on exports, boost domestic consumption and find their own model of sustainable economic growth, […] To avoid repeating developedƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ countries’ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ mistakes,ƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ newlyƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ emergingƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ economiesƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ shouldƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ investƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ inƒÆ’-¡ƒ”š‚ ƒÆ’-¡ƒ”š‚ education, technology, the environment and public health and find a sustainable model of economic growthƒÆ’‚¢ƒ¢-¡‚¬ƒ”š‚

ƒÆ’-¡ƒ”š‚ Looking inward and filling the gaps in education, technology and public health is very important in assuring that the population would not be disempowered in the face of external competition, that they are competent enough and the economic development would be sustainable. Although Sri Lanka boasts of high ranking in the Human Development Index with respect to literacy, Sri Lankan population appears to be fallen short of relevant skills to the upcoming markets such as IT and BPO. Global Services Location Index 2011 records only an insignificant amount for ƒÆ’‚¢ƒ¢-¡‚¬ƒ”¹…”peopleƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢s skills and availabilityƒÆ’‚¢ƒ¢-¡‚¬ƒ¢-¾‚¢ in Sri Lanka and the country has also fallen short of relevant experiences as well as size and availability of labour force which calls for more investments in R&D, increasing public expenditure on education and harnessing ICT sector of the country. IT/

BPO sector brings 100% value addition and has proven to be resilient even in the face of the global financial crisis.

ƒÆ’-¡ƒ”š‚ Sri Lanka is located at the 21 place and IT/BPO sector is the 5th largest export revenue earner in 2010 even after entering the market late. This sector also holds significant opportunities for future from the emerging markets such as IT sector in the Middle East.

ƒÆ’-¡ƒ”š‚ Prospective economic integration in the Indo-Pacific region, be it India going to the East in the form of an ASEAN related regime or a convergence of interests in an inter-regional platform or a brand new institutional mechanism will become a reality in the future.

ƒÆ’-¡ƒ”š‚ Therefore, small economies in the region could be attentive to the new developments in the region, engage in a critical evaluation of these developments in order to take advantage of them. Integrating more with the Indian ƒÆ’-¡ƒ”š‚ market through existing free trade arrangements, creating a unique niche for the local products, and pursuing a ƒÆ’-¡ƒ”š‚ genuine policy to harness local potential would be highly important to ensure that these economies would not be left out in the course of global developments.

ƒÆ’-¡ƒ”š‚ India on the other hand could pursue a more benevolent outward looking policy by focusing more towards its neighbouring countries and assisting to develop their economies. As the South AsianƒÆ’-¡ƒ”š‚ regionalƒÆ’-¡ƒ”š‚ powerƒÆ’-¡ƒ”š‚ IndiaƒÆ’-¡ƒ”š‚ shouldƒÆ’-¡ƒ”š‚ focusƒÆ’-¡ƒ”š‚ onƒÆ’-¡ƒ”š‚ creatingƒÆ’-¡ƒ”š‚ anƒÆ’-¡ƒ”š‚ environmentƒÆ’-¡ƒ”š‚ conduciveƒÆ’-¡ƒ”š‚ toƒÆ’-¡ƒ”š‚ resolve regional problems which obstruct the region from progressing. While it might be important to acknowledge external pressure, as the regional power it is the responsibility of India to protect the regional countries from external interferences.

ƒÆ’-¡ƒ”š‚ In conclusion, one may argue that India would be economically better off without its smaller neighbours. However, historical and cultural relations with India as well as other cross border spillovers (security and non security threats) inhibit India from taking off alone. Like I have said at the World Economic Forum in India last November pain of one nation is pain of another as we are interconnected, we should assist India to be a regional power and the surrounding countries should help India to achieve this, it’s also important that India play an active role and recognize problems of its surrounding nations. Let me end with a quotation by Mahatma Gandhi ƒÆ’‚¢ƒ¢-¡‚¬ƒ…-I do not want my house to be walled in on all sides and my windows to be stuffed. I want the cultures of all the lands to be blown about my house as freely as possible. But I refuse to be blown off my feet by any.ƒÆ’‚¢ƒ¢-¡‚¬ƒ”š‚

ƒÆ’-¡ƒ”š‚ Thank you.

March 27th, 2013 at 4:04 pm

The pain is India.